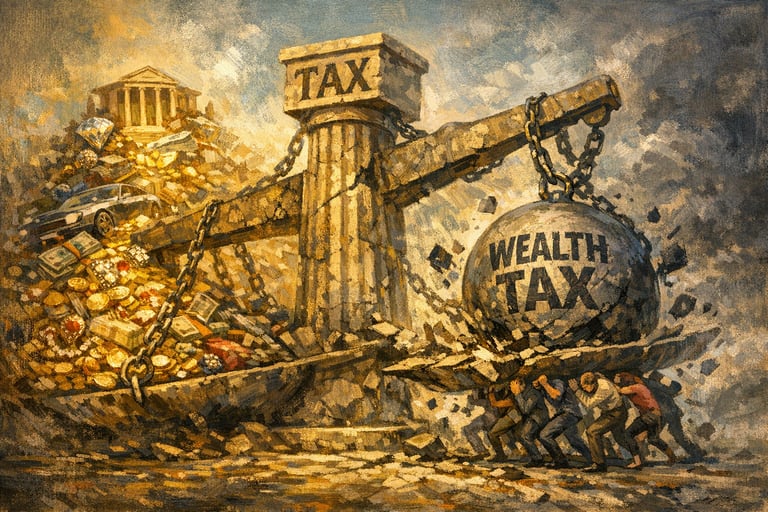

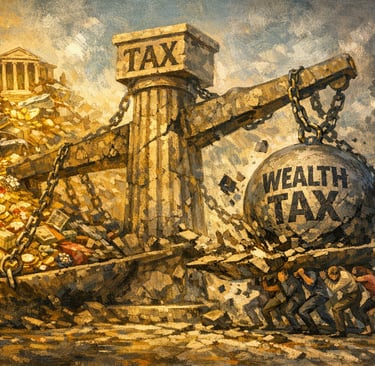

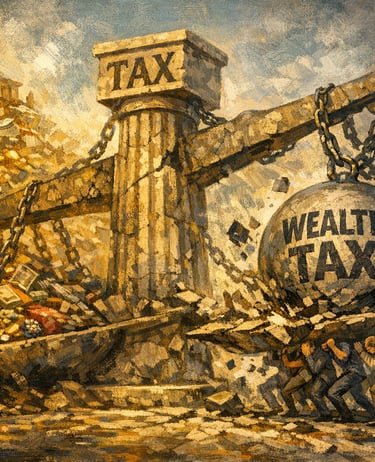

Concerning California's Wealth Tax Proposal - Part 2

Digging into the Constitutional and Practical Ramifications

BLOG

Steven A. Carlson

6 min read

To see a list of all commentaries, click the above picture.

Political Polls: Manufactured News - Part 3

Political Polls: Manufactured News - Part 2

The 27th Amendment - Prepare to Chuckle

Concerning California's Wealth Tax Proposal - Part 1

The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are reserved to the States respectively, or to the people.

Wealth Tax - Constitutional Considerations

The objective in Part 2 of this essay is to consider how a wealth tax like that currently being proposed in the state of California will be viewed when weighed against the U.S. Constitution. After all, if as anticipated the wealth tax is given a thumbs-up by California residents, it will surely be challenged by those who will be impacted. How, then, will the courts view the tax and what constitutional considerations will impact the courts’ decisions?

The 10th Amendment

An important factor when it comes to taxation of residents by individual states comes in the form of the 10th Amendment. Concerns were raised by men like Thomas Jefferson and Patrick Henry that the U.S. Constitution provided the federal government with far too much power. This amendment was intended to assuage those concerns. It reads as follows:

The basic principle outline in this amendment is that in the United States of America, the individual states should be considered autonomous: In other words, unless a particular issue required federal input or jurisdiction (i.e., foreign affairs, interstate commerce, etc.), the federal government would not involve itself in the internal workings of the states.

If this standard is applied by the courts when considering the constitutionality of a wealth tax, it is difficult to imagine the courts ruling against any state seeking to impose such a tax. However, the 10th Amendment is not the only factor that may be taken into consideration. In fact, it may not be the primary factor in such a case.

The 16th Amendment

While an income tax was utilized briefly during the Civil War to help cover the cost of the war, taxes on individuals were not really part of American history. Prior to the ratification of the 16th Amendment much of the revenue that funded the federal government was derived from tariffs on imported foreign goods. Additionally, states were responsible for collecting taxes, through sales taxes and other means, and submitting that state’s share of the cost of federal operations.

The 16th Amendment, ratified in 1913, grants the federal government the power to impose a tax on income without apportioning it among the states. The amendment reads as follows:

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

Some have suggested that this amendment might limit California’s ability to impose a tax on an individual’s wealth since it only authorizes tax on income, not on wealth. However, it may not be that simple. First, the amendment is aimed specifically at taxation imposed by the U.S. Congress. Second, while the amendment refers only to taxes based on income, the reality is that even if an argument could be made that the amendment might apply at the state level, it may not be as limiting as one might expect. Given these two factors, it is important to determine how the proposed California wealth tax might play out if it is, indeed, approved by the people of California.

The first matter mentioned in the previous paragraph concerning this amendment is that it relates only to imposition of taxes by the federal government. This begs the question: Can a state’s form of taxation be limited by this amendment? Based on a strict reading of the text, it appears that the amendment would not apply to taxation by a state. Additionally, the California Constitution does not prohibit the state from imposing a wealth tax. Consequently, the proposed California wealth tax should be able to withstand a 16th Amendment challenge on that basis.

The second issue mentioned above is that the 16th Amendment is very specific. It is designed to authorize a tax on an individual’s income. The particulars of that income tax are not defined in the amendment and, as everyone is aware, the character of the federal income tax has changed dramatically since the amendment was ratified in 1913. Still, the truth is that the 16th Amendment’s authorization to tax incomes has not deterred the federal government from imposing other taxes.

The federal government has successfully imposed a number of taxes that cannot really be categorized as income taxes. While the Social Security tax is income-based, it is not categorized as an income tax. Additionally, other taxes have been imposed that are not income-related. For instance, there are federal taxes on the sale of items like gasoline and alcohol. Also, the federal inheritance tax is not income-based, but is calculated on an estate’s value. This suggests, then, that the 16th Amendment has not served as much of a buffer between the citizenry and the federal government’s propensity to tax. Consequently, it is unlikely that this amendment might successfully overturn California’s wealth tax.

The 14th Amendment

The final constitutional amendment that may be considered in weighing a wealth tax is the 14th Amendment. While the first clause in the amendment deals with birthright citizenship, the final clause reads:

No State shall make or enforce any law which shall abridge the privileges or immunities of citizens of the United States; nor shall any State deprive any person of life, liberty, or property, without due process of law; nor deny to any person within its jurisdiction the equal protection of the laws.

How might this amendment be applied in a challenge to a wealth tax imposed by one of the states? Actually, there are arguably two principles that might be raised. The first is that a State cannot deprive a citizen/person of “…property, without due process of law.” In this instance, the court would be faced with determining whether a ballot initiative accepted by the citizenry of the state could be considered due process. It may be argued that the vast majority of those who approve the tax have nothing at risk and are yet able to determine a tax that someone else must pay. Those challenging the tax may present this as a lack of due process. Still, it seems highly likely that courts would find in favor of the state on that issue.

The second question raised by this amendment is whether all people in that jurisdiction are being provided “equal protection.” Indeed, this clause may present an issue in defending wealth tax. An argument might be made by the state that a wealth tax operates as a property (real estate) tax, but that is a difficult position to support. When it comes to real estate taxes, everyone who owns real estate within the jurisdiction is required to pay. In fact, even those who do not directly own property (renters) participate in that a portion of the rent is designated as property tax.

The difficulty under the equal protection clause is that a particular sector of the population is being singled out to pay what is essentially a high-end property tax. Indeed, if a state sought to charge property taxes only on real estate valued above $1 million, this clause could be problematic. It could be, then, that the court would find against the tax unless it includes 5% of the net assets of everyone in that jurisdiction.

Courts can be unpredictable, and this is one of those topics where the outcome is difficult to forecast. Strong arguments may be introduced by both sides. What is not difficult to foresee, however, is the prospect of taxation in the U.S. if California is indeed successful in its effort to implement such a tax. Come back for Part 3 where the future of taxation will be viewed through the lens of a successful California wealth tax.

End Part 2

------------------------------------------------------------------------------If you enjoyed this article, please encourage your friends to visit us here at constitutionmatters.net where the Constitution really does matter.

See below for contact information

This book will truly enhance your understanding of the Declaration of Independence and the United States Constitution. Click the button below to check it out.

___________________________________________________________________________________________________________________________________________________________________________________________________

Contact

Questions? Reach out anytime.

Email:

contact@constitutionmatters.net

© 2025. All rights reserved.