Is Social Security a Ponzi Scheme?

Considering the Character of the Program

Steven A. Carlson

12 min read

To see a list of all commentaries, click the above picture.

Birthright Citizenship and a Typhlotic Courtroom - Lesson 5: 20th Century U.S. Citizenship

Birthright Citizenship and a Typhlotic Courtroom - Lesson 6: Oral Arguments

DJ Trivia and the Problematic Preamble

Proposal for the 28th Amendment

The allegation has been made, perhaps most notably by Elon Musk in early 2025, that the Social Security System managed by the federal government as a purported retirement safeguard for seniors is, indeed, a Ponzi scheme. Of course, Musk is not the first to make the claim, nor will he be the last. It begs the question: Exactly what is a Ponzi scheme? After all, how can anyone determine the veracity of Musk’s remarks without identifying the nature of a Ponzi scheme? According to brittanica.com:

A Ponzi scheme sounds like a real potential money-maker, at least for the originator of the operation and for early investors. First you find a few individuals to invest in a plan promising high returns. You then take more money from people who are impressed by the returns and use their money to reward the earliest investors. The gains encourage even more investors whose money is then used to profit second-tier investors. What a plan!!!!! In fact, it is an incredible operation that pays huge profits…until it doesn’t. Eventually the “new” investors will begin to dry up. Once that happens payouts to investors dry up. Then it’s over and the originator walks away with whatever money he/she has been able to skim off the top, which is usually substantial.

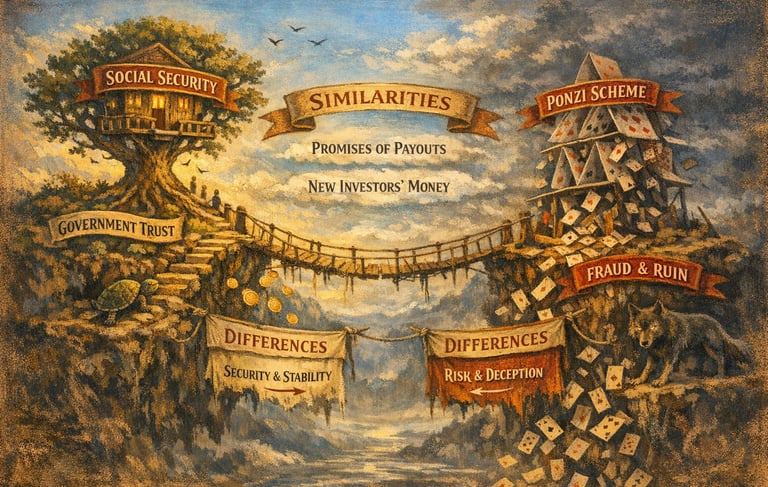

Elon Musk and others have likened the U.S. Social Security System to a Ponzi scheme. Here we will consider the similarities and differences between the two. Also included will be a discussion of the constitutionality/unconstitutionality of Social Security as well as other government-run social programs generally.

Many Americans have a major misapprehension where Social Security is concerned in that they look at the money withheld from their paychecks (labeled FICA on their check stub) as a type of savings that is being set aside by the government in an account for their retirement. That is not the case. The money that is withheld from current employees actually goes directly to the bank accounts of those who have been determined to be eligible recipients of Social Security.

Social Security was initially withheld from employees’ paychecks beginning in January 1937. At the time, employees paid 1% of their first $3,000 in earnings ($30 per year per person). The first individual to draw from Social Security in retirement was a woman by the name of Ida May Fuller who received that first payment on January 31, 1940. She received $22.54 monthly at the time. However, prior to her retirement, Ida had paid a total of $24.75 into the system. Consequently, she was not receiving payments from a savings account into which she had paid over the years. She was being paid from the withholdings of those who were still working. Over the course of her retirement, Ida received a total of $22,888.92 in Social Security payments by the time she passed away in 1975.

Given this example, it is easy to see why Elon and others would refer to Social Security as a Ponzi scheme. It works much like a Ponzi scheme. Money currently being withheld from individuals’ paychecks (new investors in a Ponzi scheme) is paid directly to those who have already retired. It does not go into savings accounts for the current contributors even though it is credited to the employees’ Social Security accounts. That credit is tracked only to determine how much each person will receive from the paychecks of others upon retirement.

Differences

The most obvious difference between Social Security and a Ponzi scheme is that Social Security is government-run and, as such, has the backing of the full faith and credit of the U.S. government. Some may either laugh (or cringe) at that notion given the history of our politicians’ handling of money. Indeed, that laugh (or cringe) may well be justified. Still, this is a distinguishing characteristic of Social Security when weighed against a Ponzi scheme.

An additional rather obvious difference is Social Security’s compulsory participation. In a Ponzi scheme, no one is forced to invest. Participation is purely voluntary. Consequently, investors must be persuaded to participate. In contrast, Franklin Roosevelt’s New Deal, which was passed into law in 1936, generally compelled each working person in the United States to contribute to the system from wages earned.

An additional difference between Social Security and a Ponzi scheme is transparency. In a Ponzi scheme, an individual is lured into an investment trap with promises of significant (often unrealistic) financial returns. However, those returns are not real and the true nature of the scheme is well-hidden from the potential investor. Unlike a Ponzi scheme, participants of Social Security are aware that their payments go into a system from which they can expect to receive payments in the future based on specific mathematical formulae. There is no promise of unrealistic financial rewards.

A Ponzi scheme eventually collapses when the pool of new investors is depleted. Consequently, those who got in early are rewarded while those who invested late generally lose their total investment. Social Security works differently in that what a person receives in retirement is based on that person’s earnings over the course of their working life. Some individuals like Ida May Fuller, because they end up living perhaps thirty years beyond retirement, will end up collecting far more than they ever paid into the system. Other individuals, whose lives are cut short, may receive far less than they paid in. Indeed, someone who dies prior to retirement will not collect a monthly retirement payment from the system even though their contribution was sizable.

Similarities

The primary similarity between social security and a Ponzi scheme is that, like a scheme where the money from new investors is used to pay previous investors, there is no actual investment. It is purely a transfer of funds from one group of individuals (workers) to another group of individuals (retirees). Applying a seemingly respectable title like “Social Security” does not change the nature of the beast. After all, attaching the title of “Lottery” to a government-run program to raise money does not change the fact that it is still gambling.

Another dire similarity between Social Security and a Ponzi scheme is that they are both unsustainable in perpetuity. At least, the way Social Security is currently run combined with increased life expectancy in the United States, it is unsustainable. Just as a Ponzi scheme will eventually run out of new investors, there will come a point in time when current workers will not be able to supply the funds needed to support retirees under the Social Security System. There are a number of reasons for this, which will be discussed shortly.

The State of Social Security

Experts have indicated, based on actuarial numbers, that the Social Security Fund will run dry in the year 2033 if not before. That is a mere seven years down the road. It begs the question: What will happen when the fund runs out of money? This is especially disconcerting since Congress has known about the coming shortfall for at least the last three decades and yet, has done little to address the problem.

Currently, employees pay into the Social Security System 6.2% of their annual earnings, maxing out when earnings reach $184,500. This maximum wage is increased annually. Additionally, the employer matches that number, paying 6.2% of the employee’s wages into the system. The current average annual wage in America is roughly $62,000. An employee earning $62,000 would pay $3,844 into the system for the year and that person’s employer would also pay in $3,844. Considering the average retiree receives $23,040 annually in Social Security payments, it currently takes roughly three average workers to support the average retiree. In 1960 it took roughly five workers to support the average Social Security recipient. It seems obvious that this trend is not sustainable.

One step Congress has taken lately is to increase the retirement age when a person is eligible to receive full Social Security benefits. The original age in the 1930’s was 65. However, in 1983, the age for full Social Security benefits began to rise ever so slowly. That age is now 67. Yet, even with this adjustment, the fact is that it now takes three workers to support a Social Security recipient, so this step alone is clearly insufficient.

How We Got Here

There are a number of reasons the Social Security Fund is facing the quickly-approaching shortfall. Part of the shortfall is due, of course, to the very pyramid foundation upon which Social Security was built. As individuals live longer, it takes more money to support those recipients. This is something discussed earlier and it is a trend that will continue into the foreseeable future. However, other factors have contributed to the predicament the Social Security Fund is facing.

It is understandable that the population growth suffered during the 1930’s while in the throes of the Great Depression. However, the U.S. saw substantial (double-digit) growth annually between 1940 and 1980. With the exception of the 1990’s, the U.S. growth rate has declined each of the last six decades. Additionally, the percentage from 2020 thru 2026 translates into another decline in the current decade.

While people born in the 1940’s, 1950’s, and 1960’s are now mostly retired or retiring and receiving Social Security benefits, it is people born between 1970 and 2000 who are now in the work force. The graphic suggests that those numbers do not bode well for the Social Security program.

4. There is a related topic that may partly explain the decline in population growth over the last few decades. It is said that since the Supreme Court’s 1973 decision legalizing abortion, roughly 65 million abortions have taken place in the United States. Absent those abortions, imagine the money that would have flowed into the Social Security system if even half of those who were aborted had contributed to the system beginning in the early 1990’s. Millions of people would have been added to the workforce over the past thirty years. It is safe to say that the reduced workforce is at least partly responsible for the shortage of Social Security funds.

5. Longevity is another reason Social Security is in trouble. In the 1930’s, the average life span for men was 58 years. For women, it was 62 years. In the 1940’s life expectancy was 60.8 years for men and 65.2 years for women. In 2026 those numbers have risen to 76.5 years for men and 81.4 years for women. It is easy to see how these numbers have impacted the Social Security fund. The longer people live, the longer they collect Social Security.

Social Security and the U.S. Constitution

The Great Depression, starting in 1929, led to Franklin D. Roosevelt taking over from Herbert Hoover as U.S. President in 1933. Roosevelt felt the federal government should play a hands-on role in reviving the economy, so between 1933 and 1937, Congress passed his New Deal plan. This included public works projects, banking reforms, Social Security, and other programs aimed at economic recovery.

The Supreme Court rejected many of Roosevelt’s proposals, arguing they went far beyond the constitutional limits on the federal government, with the 10th Amendment playing a key role in those rulings. Still, after his landslide reelection in 1936, Roosevelt used his political clout to threaten expanding the Court with justices who would support him. This move led to the 10th Amendment being sidelined and most New Deal programs going into effect.

It probably won’t shock you to hear me say that Social Security, along with many other social programs, is unconstitutional. After all, the U.S. Constitution doesn’t grant the federal government the authority to create such programs, and the 10th Amendment explicitly prohibits it, stating:

A Ponzi scheme is a type of pyramid scheme in which the operator, at the pyramid’s top, acquires a small group of investors that is initially provided with tremendous investment returns via funds secured from a second group of investors. The second group, in turn, is paid with funds obtained from a third group of investors, and so on until the number of potential investors is exhausted and the scheme collapses.[1]

1. When the Social Security program was initially developed, it was designed as a retirement safeguard, assuring that people who contributed to the fund would have at least a small income upon retirement. However, in the early stages of the program, it was determined that dependents of a deceased individual – particularly his/her children – should benefit from the money that person had paid into the system. This is known as survivor benefits. Consequently, the system broke the constraint of serving strictly as a retirement benefit, adding substantially to the cost of the program.

2. In 1956, Congress amended the Social Security Act. At that time, it was decided that a person who paid into the system and then became disabled and was unable to work should receive Social Security benefits at the time of disability. Needless to say, this added considerable costs to the program.

3. The U.S. has experienced a significant decline in population growth over the last century. Consider these numbers:

The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are reserved to the States respectively, or to the people.

Decade U.S. Growth Rate

1920-1930 16.2%

1930-1940 7.4%

1940-1950 14.5%

1950-1960 19.0%

1960-1970 13.4%

1970-1980 11.4%

1980-1990 9.8%

1990-2000 13.2%

2000-2010 9.7%

2010-2020 7.4%

2020-2026 3.1%

This amendment is written with true clarity. Since the Constitution does not delegate that power to the federal government, the government lacked the authority to establish such a program. Unfortunately, that is water under the bridge as the citizenry has come to rely on the program over the last century.

What Is Next for Social Security?

Social Security currently runs a shortage of $250 billion annually, spending $1.6 trillion while receiving $1.35 trillion. That is a nearly 16% shortage each year. It’s difficult to say how Congress will deal with the coming Social Security shortfall, but the options are few. Here are some possibilities:

1. Raise Social Security Taxes: This one seems obvious, but it may not be palatable where the public is concerned. The increase would necessarily be substantial – perhaps an increase from 6.2% of wages to 7.2%.

2. Establish a New Tax: Congress could develop a new tax – perhaps a sales or excise tax – with the funds designated specifically for the Social Security System.

3. Reduce payments to recipients of Social Security: However, to make the necessary impact, that reduction would likely have to be in the 16% range. While it would be unwise, and certainly unpopular, to reduce payments to current recipients, the formula for determining benefits could be adjusted downward each year for future recipients. Over the course of time the savings would be significant.

4. Increase the age at which a person may collect Social Security: Currently, an individual may begin receiving Social Security payments as early as age 62, albeit at a reduced rate. The age at which someone may receive their full retirement benefit is 67. Congress could increase the age at which a person may initially receive retirement income to, say, 65 and continue to increase the age at which full retirement benefits are available. This would undoubtedly provide substantial savings for the program.

5. Use a combination of ideas: Congress could, of course, employ a combination of these ideas, reducing the impact from a single approach.

Needless to say, these measures would not fix the issues with Social Security. The resemblance to a Ponzi scheme is too profound and, as it exists, a program like Social Security is not sustainable. Ultimately, it seems work should begin on a system requiring individuals to set aside a certain percentage of their income each year for retirement. Yes, that would be unconstitutional since the Constitution does not provide the government the authority to make such a requirement. However, where Congress is concerned, unconstitutionality has proven to be an ineffectual deterrent over the past 250 years.

________________________

[1] Britannica Money, britannica.com, accessed April 18, 2026

------------------------------------------------------------------------------If you enjoyed this article, please encourage your friends to visit us here at constitutionmatters.net where the Constitution really does matter. Also, if you appreciate the articles and insights provided here, feel free to contribute to the cause by clicking below.

This book will truly enhance your understanding of the Declaration of Independence and the United States Constitution. Click the button below to check it out.

___________________________________________________________________________________________________________________________________________________________________________________________________

Feel free to visit restoretheword.com

Contact

Questions? Reach out anytime.

Email:

contact@constitutionmatters.net

© 2025. All rights reserved.